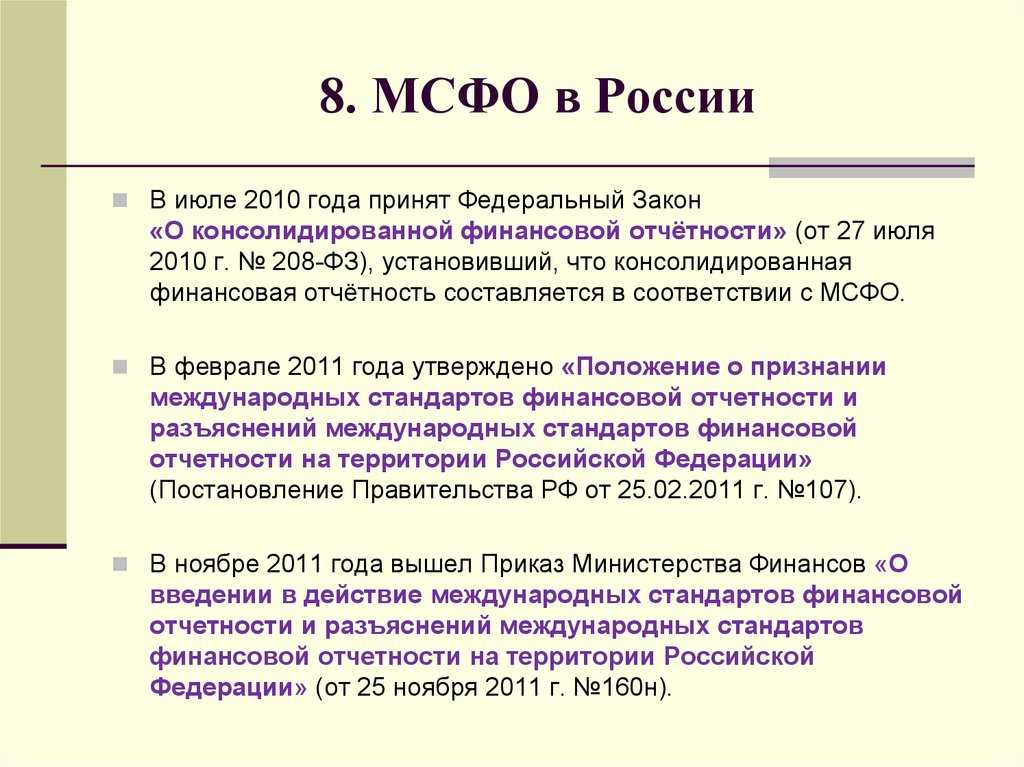

Какие выгоды у банков от перехода на МСФО?

Привлечение иностранных инвестиций

Представим, что вы — собственник банка — приняли решение расширить бизнес и привлечь средства иностранных инвесторов. Как заинтересовать будущего вкладчика? Во-первых, вы должны

понимать друг друга на уровне символов и разговаривать на одном языке. В данном случае этот язык — МСФО. Он поможет вам наглядно продемонстрировать финансовые результаты вашей

деятельности, а также доказать, что именно ваш бизнес более привлекательный по отрасли на международном рынке.

Сотрудничество с иностранными партнерами

Если вы уже работаете с зарубежными контрагентами, наверняка знаете, что финансовые показатели банка на собраниях директоров представляются по международным стандартам финансовой

отчетности или по корпоративным стандартам компаньонов, приближенным к международным.

Повышение прозрачности бизнеса

Порой бизнес становится менее наглядным и запутанным, когда в вашем распоряжении находится несколько банков. Понять реальную картину, рассчитать величину прибыли и выяснить

результаты деятельности поможет консолидированная отчетность.

Управленческие цели

Когда вы поставили цель улучшить управленческую отчетность и повысить эффективность работы банка, МСФО намного превосходят национальные стандарты. Они упрощают регулирование и

упорядочение всех операций, а также являются знаком качества управленческого учета.

How to measure financial instruments?

Initial measurement

Financial asset or financial liability shall be initially measured at:

- Fair value: all financial instruments at fair value through profit or loss;

- Fair value plus transaction cost: all other financial instruments (at amortized cost or fair value through other comprehensive income).

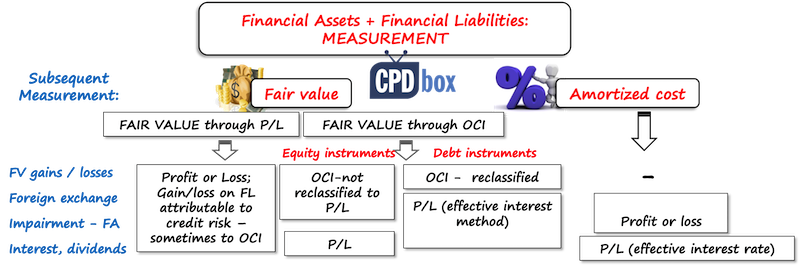

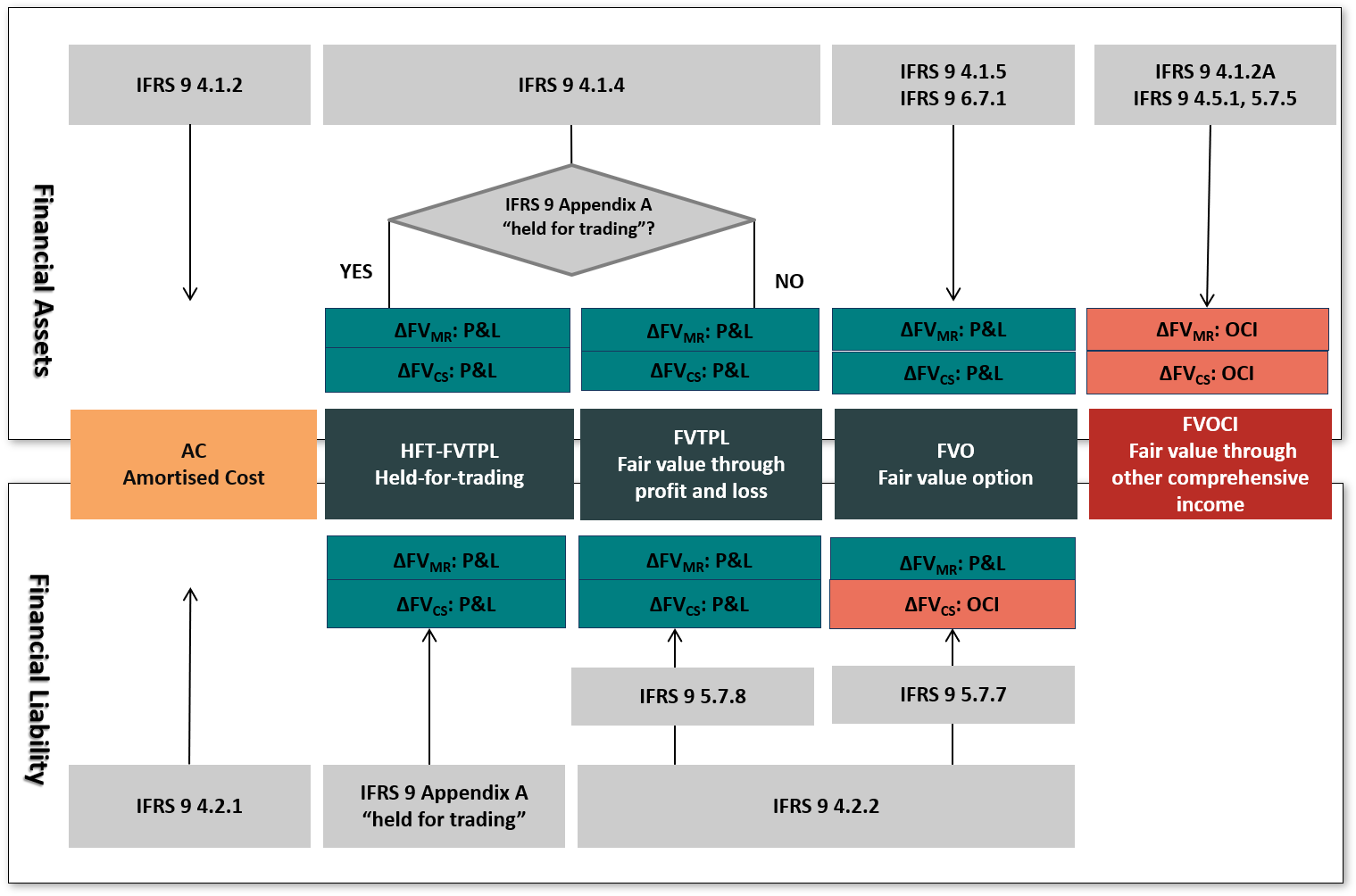

Subsequent measurement

Subsequent measurement depends on the category of a financial instrument and I think it’s self-explanatory according to the title of a category:

- Financial assets shall be subsequently measured either at fair value or at amortized cost;

- Financial liabilities are measured at amortized cost unless the fair value option is applied.

With regard to recognizing gains and losses from subsequent measurement, here’s the scheme for your convenience:

Impairment of financial assets

This is exactly the most important part for all of you who “have no financial instruments in their financial statements”.

Why?

Because, I explained above, even trade receivables are financial instruments.

Are you booking the bad debt provision?

So here you go.

Using the IFRS 9 terminology, “bad debt provision” = impairment of financial assets, or a loss allowance.

The new rules about the impairment of financial assets were added only in July 2014.

It does NOT affect all financial assets. For example, shares and other equity instruments are excluded, because their potential impairment is taken into account when re-measuring these investments to their fair value.

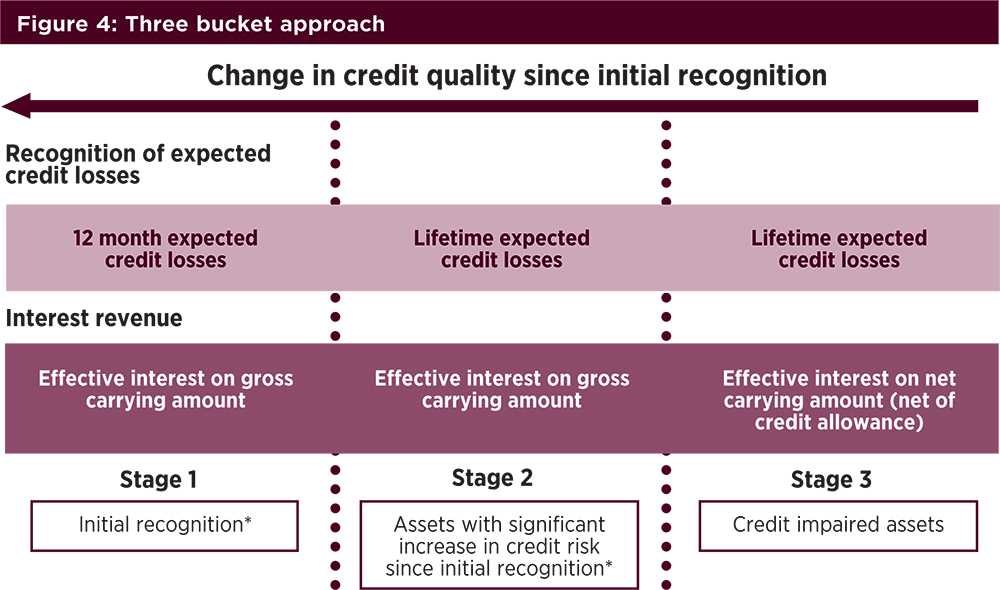

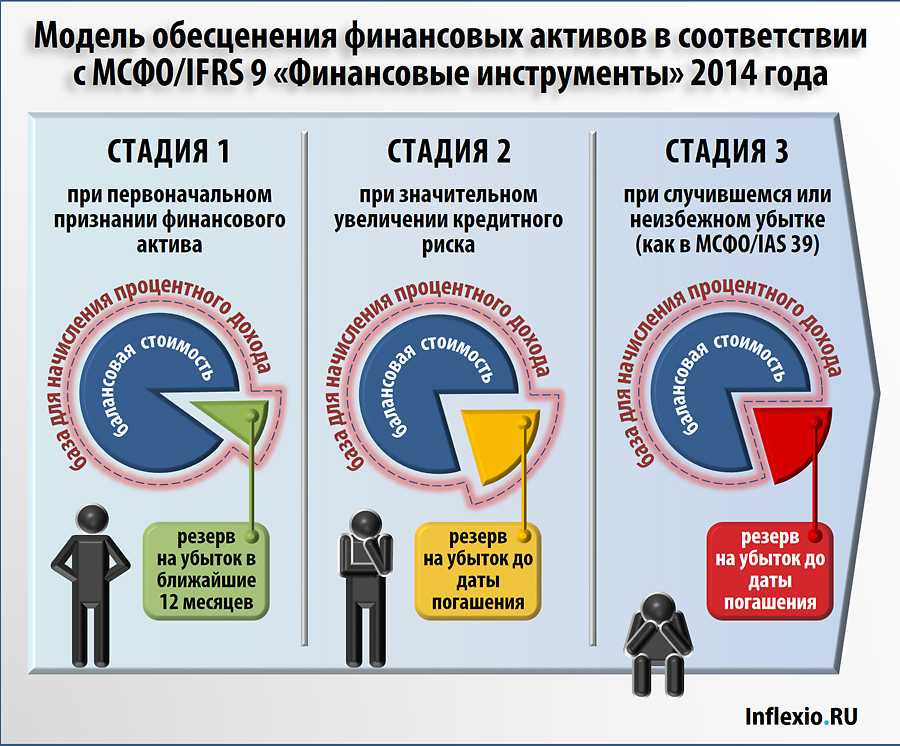

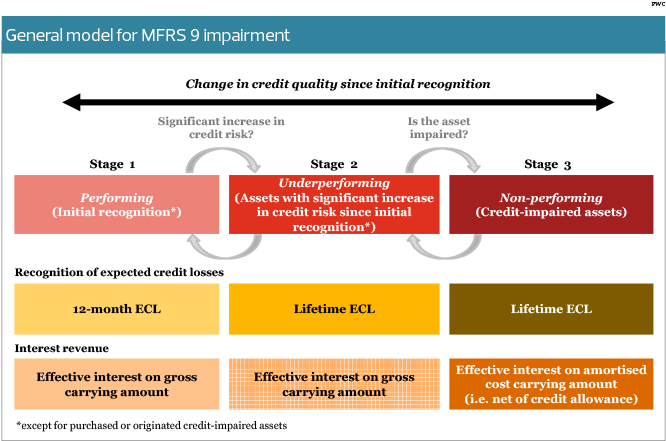

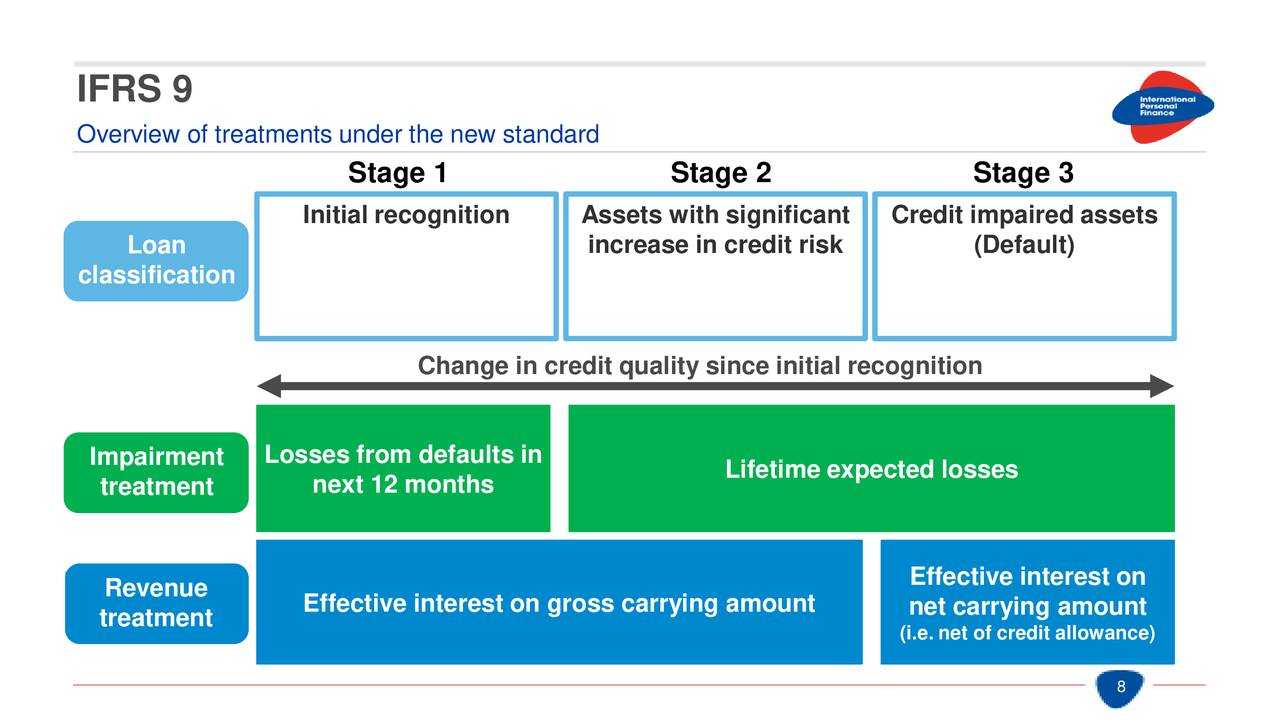

IFRS 9 requires entities to estimate and account for expected credit losses for all relevant financial assets (mostly debt securities, receivables including lease receivables, contract assets under IFRS 15, loans), starting from when they first acquire a financial instrument.

When measuring expected credit losses, entities will be required to use all relevant information that is available to them (without undue cost or effort).

IFRS 9 offers two approaches:

-

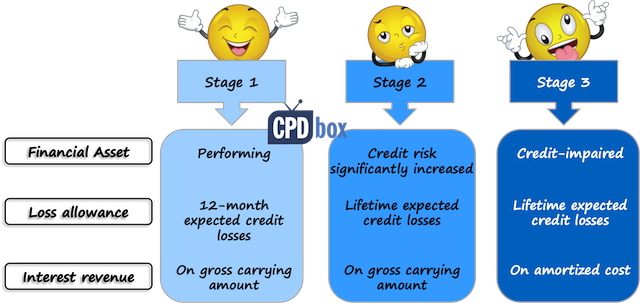

General model for measuring a loss allowance:

This model recognizes loss allowance depending on the stage in which the financial asset is. There are 3 stages:- Stage 1 – Performing assets: Loss allowance is recognized in the amount of 12-month expected credit loss;

- Stage 2 – Financial assets with significantly increased credit risk: Loss allowance is recognized in the amount of lifetime expected credit loss, and

- Stage 3 – Credit-impaired financial assets: Loss allowance is recognized in the amount of lifetime expected credit loss and interest revenue is recognized based on amortized cost.

-

Simplified model:

You don’t need to determine the stage of a financial asset, because a loss allowance is recognized always at a lifetime expected credit loss.

If you subscribe to the free newsletter, you’ll receive an exclusive article with the video about the new impairment model.

Financial guarantees vs other guarantees

IFRS 9 defines a financial guarantee as ‘a contract that requires the issuer to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payment when due …’. Such financial guarantees fall within the scope of IFRS 9 and are accounted for as described . It’s essential to note that not all contracts legally labelled as ‘guarantees’ qualify as financial guarantees under IFRS 9. The above definition is relatively narrow and only covers payments made when a debtor defaults on their payment. For a more comprehensive discussion, refer to IAS 32.AG8.

There are other types of ‘guarantees’, which despite being contractual financial instruments, do not fall under the category of financial guarantees. Depending on their nature, these can be treated as or derivatives and accounted for under IFRS 9, or as insurance contracts under IFRS 17 (see below). For instance, PWC believes that performance guarantees not satisfying the definition of an insurance contract should be accounted for as loan commitments (see this discussion on our forums).

IFRS 17 defines an insurance contract as ‘a contract under which the issuer accepts significant insurance risk from the policyholder by agreeing to compensate the policyholder if a specified uncertain future event adversely affects the policyholder’. Insurance risk refers to any risk that is not financial risk (see IFRS 17 Appendix A). For further insights on this topic, refer to paragraphs IFRS 17.B7-B16 and this Deloitte’s publication on the applicability of IFRS 17 to non-insurers.

Note that it is incorrect to account for contractual guarantees under IAS 37 as this standard does not cover financial instruments.

Сложности перехода

Переход на IFRS 9 связан с некоторыми трудностями. Например, британская ассоциация банкиров сравнила трансформацию учета с переключением на общий стандарт МСФО. К основным сложностям они отнесли:

- процесс преобразования ведения бухгалтерского учета;

- внедрение новой модели расчета ожидаемых кредитных убытков;

- регулирование динамики доходности и ключевых показателей эффективности;

- согласование отчетности с методическими рекомендациями по формированию документации с целью банковского регулирования, а также с целью учета хеджирования и работы по урегулированию рисков.

Все дело в том, что учет согласно некоторым положениям МСФО, например, бизнес-модели или договорного денежного потока, не входит в компетенцию бухгалтерского отдела. Для выявления данных показателей руководству придется нанимать специализированный персонал.

Надо отметить, что в рамках учета доходов и обесценения, между положениями IFRS 9 и методическими рекомендациями по формированию документации с целью банковского регулирования (Базель 3), имеются некоторые разногласия. В связи с этим, при составлении отчетности компании нужно согласовывать данные положения, чтобы не было нестыковок. Такие несоответствия чаще всего возникают между бухгалтерским учетом и управлением капиталом.

| Оценка стоимости бизнеса | Финансовый анализ по МСФО | Финансовый анализ по РСБУ |

| Расчет NPV, IRR в Excel | Оценка акций и облигаций |

Учетная политика банка по МСФО: утверждать новую или работать по старой?

Согласно МСФО 8,

учетная политика — это конкретные принципы, основы, соглашения, правила и практика, принятые предприятием для подготовки и представления финансовой отчетности.

Учетная политика должна быть обязательно утверждена банком или другим уполномоченным органом кредитной организации в виде отдельного документа. Однако нет необходимости

утверждать ежегодно новую версию учетной политики. При необходимости вносите изменения в ранее действовавшую.

Вне зависимости от того, что банки уже не первый год знакомы с международными стандартами финансовой отчетности, разработка учетной политики все равно вызывает некоторые

трудности у банковских работников.

Учетная политика банковской организации не может вечно быть неизменной в течение всего срока ее деятельности. Поэтому время от времени под влиянием определенных факторов

кредитные организации подвергают изменениям учетную политику.

Внутренние факторы изменения учетной политики банка

- трансформация финансовой деятельности;

- преобразование хозяйственной деятельности.

Главными характеристиками учетной политики являются ретроспективность и перспективность применения основных изменений.

При перспективном применении учетной политики все нововведения касаются учета операций, событий и условий, которые имели место после даты введения изменений. К предыдущим

периодам пересчет и корректировка не применяются.

При ретроспективном применении учетной политики банковским специалистам приходится пересчитывать и корректировать абсолютно все показатели финансовой отчетности за предыдущие

периоды.

При выполнении такой трудоемкой работы основными сложностями, с которыми сталкиваются кредитные организации, являются:

- информирование пользователей об основных принципах применения учетной политики в отчетном периоде;

- учет всех изменений, касающихся предыдущих периодов;

- ретроспективный пересчет данных, исправление ошибок;

- результат изменений учетной политики и их влияние на показатели отчетности;

- корректное представление показателей финотчетности с изменениями и раскрытие соответствующей информации в примечаниях.

Проблемные зоны, с которыми столкнутся банковские организации во время перехода на МСФО:

- изменения в методологии учета и отчетности;

- трансформация бизнес-процессов и учетных систем;

- изменения в классификации и оценке финансовых активов;

- искажения волатильности показателей прибыли или убытка за период и собственного капитала;

- правки ключевых показателей результативности;

- уровень резервов будет сильно зависеть от состояния экономики;

- усложнение системы оценки убытков, которая будет оперировать большими объемами данных для составления прогнозов;

- реализация агрегированного расчета на основе большого объема данных, особенно для розничного портфеля.

Чтобы «выжить» во время реформ и трансформаций финансовым институтам понадобится внушительная помощь акционеров или серьезное вмешательство центрального банка в процесс внедрения

МСФО 9. Центральный банк в этом случае может перенести сроки обязательного перехода или вовсе отменить составление отчетности по международным стандартам для не системно значимых

банков.

Изучите МСФО, чтобы помочь компании перейти на МСФО-отчетность быстрее!

Пройдите комплексный курс «ДипИФР. Гарантия», чтобы освоить теорию и практику МСФО и подготовиться к официальному экзамену на диплом АССА DipIFR (rus).

Зарегистрируйтесь и пройдите 3 пробных занятия курса бесплатно!

Перейти к курсу «ДипИФР. Гарантия»

С какой проблемой чаще сталкиваются банки при переходе на МСФО?

Embedded derivatives

An embedded derivative is simply a component of a hybrid instrument that also includes a non-derivative host contract.

Accounting of embedded derivatives depends on WHAT the host contract is:

- If host = financial asset within the scope of IFRS 9, then the whole hybrid contract shall be measured as one and not separated.

- If host = financial liability within the scope of IFRS 9 OR a contract outside the scope of IFRS 9 (e.g. service contract, lease contract…), then you should separate when the conditions are met.

Special For You!

Have you already checked out the IFRS Kit ? It’s a full IFRS learning package with more than 40 hours of private video tutorials, more than 140 IFRS case studies solved in Excel, more than 180 pages of handouts and many bonuses included. If you take action today and subscribe to the IFRS Kit, you’ll get it at discount! Click here to check it out!

If an entity is not able to do this, then the whole contract must be accounted for as a financial instrument at fair value through profit or loss.

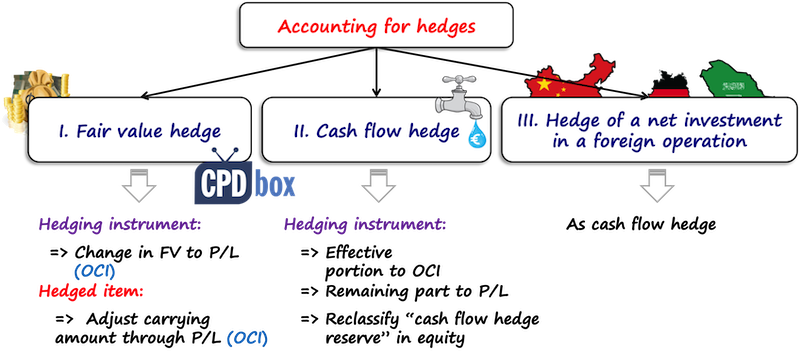

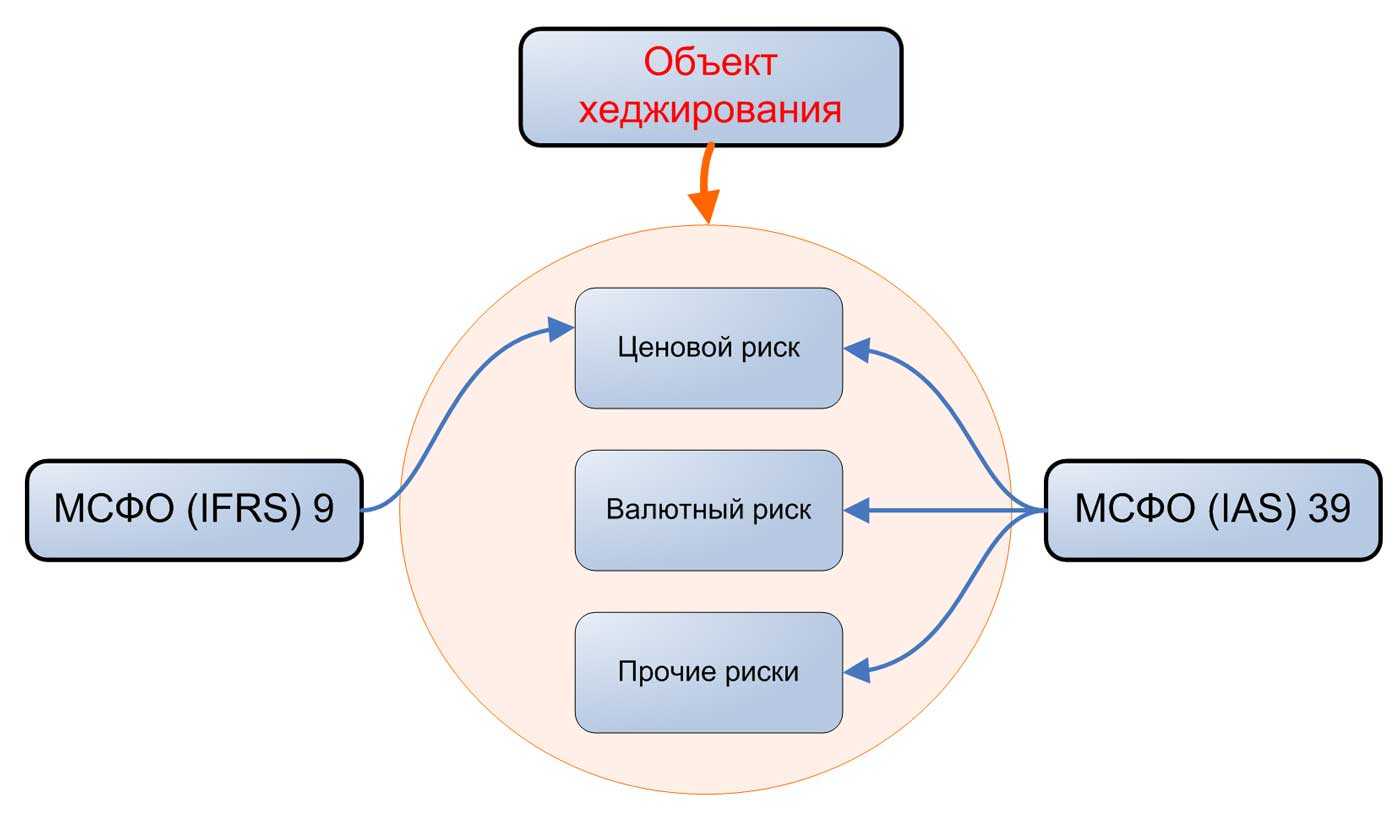

Hedge accounting

Hedge accounting is designating one or more hedging instruments so that their change in fair value is an offset to the change in fair value or cash flows of a hedged item.

If you’d like to see a simple illustration, please watch the video below this article (somewhere around the minute 17:43).

One very important remark:

Hedge accounting is NOT mandatory!

You do NOT have to do it, only if you want to (+meet the conditions).

Let’s say you try to protect your company against foreign currency risk and you enter into foreign currency forward contract. Even if you meet the conditions for the hedge accounting, you can still measure the derivative at fair value through profit or loss and not apply hedge accounting – up to you.

But, I strongly recommend reading the article about how ignoring hedging can hurt your business – maybe you’ll want to apply it voluntarily then.

If you want to apply hedge accounting, 3 criteria must be met (IFRS 9, par. 6.4.1):

- There are only eligible hedging instruments and eligible hedged items in the relationship;

- You have the hedge documentation at the inception of the hedge, in which you designate and describe your hedging,

- Hedge effectiveness criteria are met.

IFRS 9 sets the rules for 3 types of hedges:

- Cash flow hedge,

- Fair value hedge, and

- Hedge of the net investment in the foreign operation.

The overview of the accounting for these hedges is shown in the following scheme:

You can read more about hedging in one of our articles referred to below.

Firm commitments (executory contracts)

Firm commitments to purchase or sell goods or services often result in potential assets and liabilities. However, these are generally not recognised until one party has fulfilled their part of the agreement. Such commitments are often referred to as ‘executory contracts’. For instance, a firm order does not lead to the recognition of an asset or a liability at the time of commitment. Instead, recognition is delayed until the ordered goods or services have been delivered or provided (IFRS 9.B3.1.2(b)).

If a firm commitment qualifies as a derivative instrument under the scope of IFRS 9, separate provisions apply (IFRS 9.B3.1.2(b)-(d)).

Regular way purchase or sale of financial assets (trade date and settlement date)

A ‘regular way purchase or sale’ refers to the purchase or sale of a financial asset where the terms of the contract necessitate delivery of the asset within the time frame typically established by regulations or convention in the relevant marketplace (IFRS 9 Appendix A). This method is commonplace in major stock exchanges, where transactions are settled a few days after their initiation. However, the policy choice discussed here also applies to privately issued financial instruments (IFRS 9.IG.B.28).

IFRS 9.3.1.2 offers a policy choice for such transactions: they can be recognised and derecognised using either trade date accounting or settlement date accounting.

The trade date is when an entity commits to buying or selling an asset. Trade date accounting involves the recognition of an asset to be received, and the liability to pay for it, on the trade date. It also includes the derecognition of an asset that is sold, the recognition of any gain or loss on disposal, and the recognition of a receivable from the buyer for payment on the trade date. Generally, interest doesn’t start accruing on the asset and corresponding liability until the settlement date when the title transfers (IFRS 9.B3.1.5).

The settlement date is the date when an asset is delivered. Settlement date accounting refers to the recognition of an asset on the day it is received by the entity, and the derecognition of an asset and recognition of any gain or loss on disposal on the day it is delivered by the selling entity. If settlement date accounting is used, any change in the fair value of the asset to be received between the trade date and the settlement date is accounted for in the same way as the acquired asset (IFRS 9.B3.1.6).

Paragraphs IFRS 9.IG.D.2.1-3 provide examples illustrating the application of trade date and settlement date accounting. Both methods yield the same impact on P/L or OCI, with the only difference being the timing of recognition of the underlying financial asset.

The same method should be consistently applied for all purchases and sales of financial assets that are classified similarly under IFRS 9 (IFRS 9.B3.1.3). Regardless of the chosen approach, the trade date should be considered the date of initial recognition for applying the impairment requirements (IFRS 9.5.7.4).

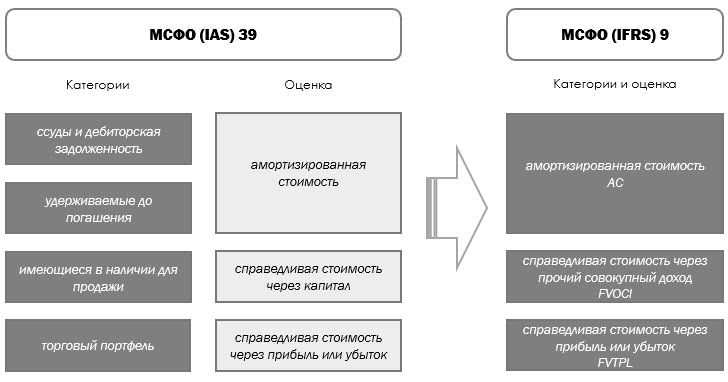

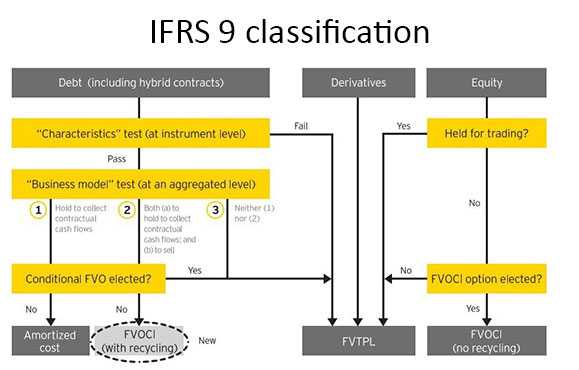

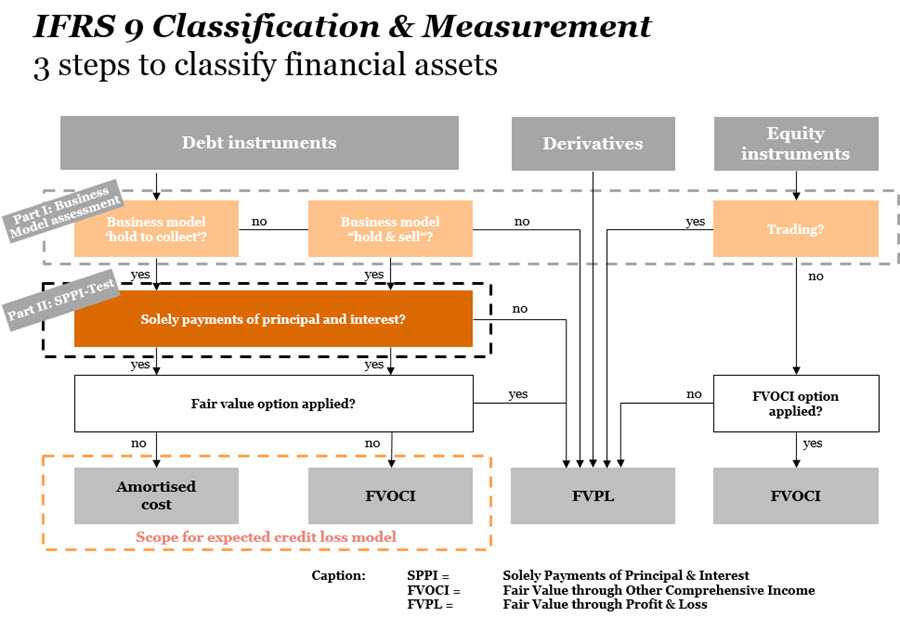

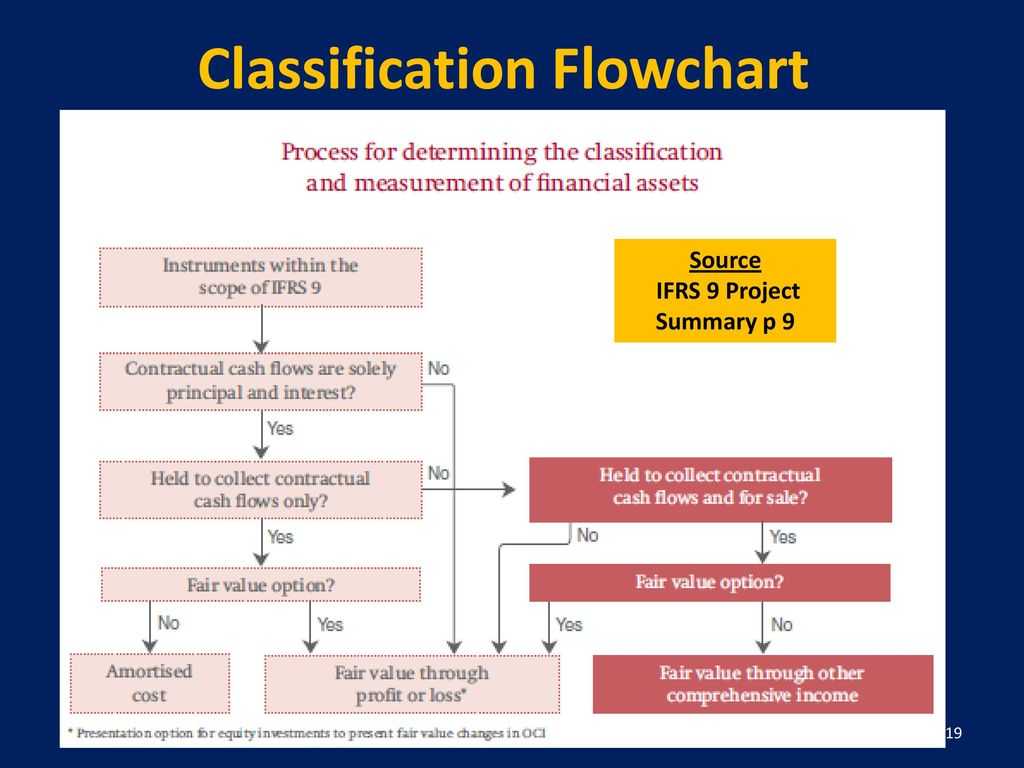

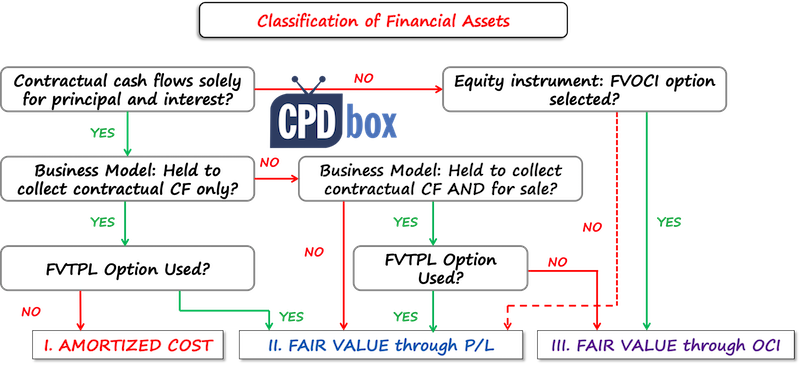

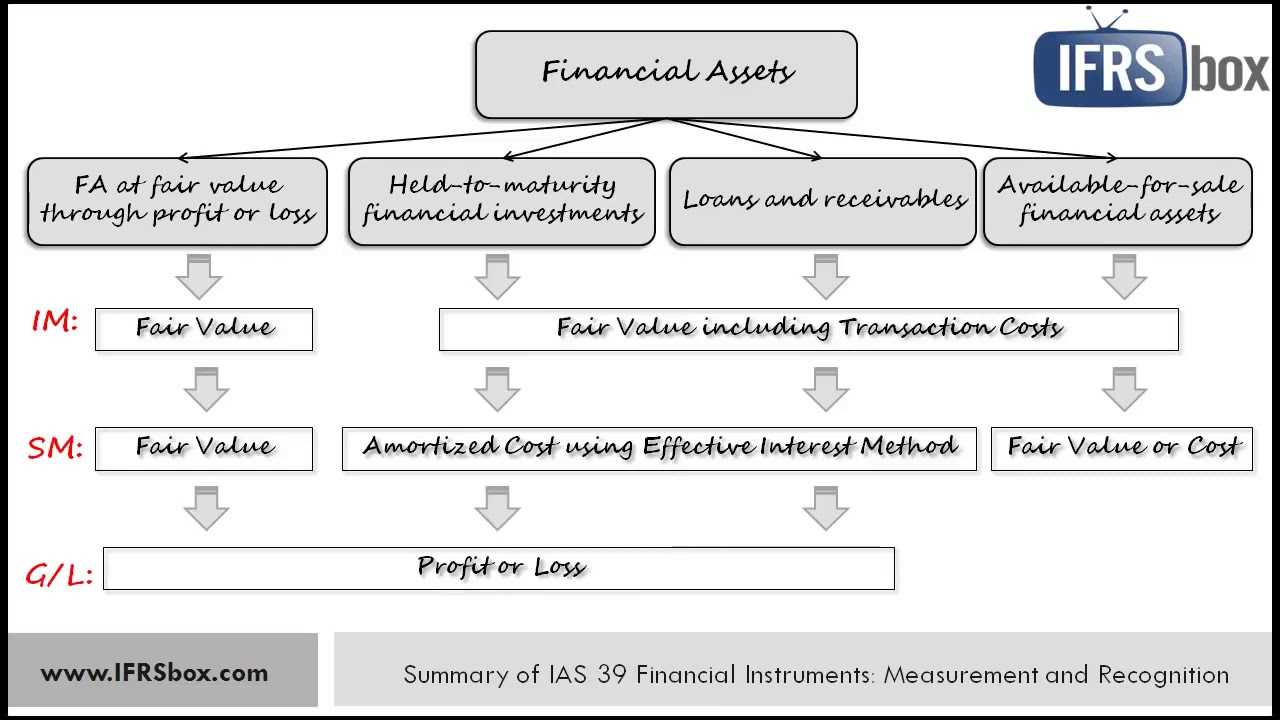

Classification of financial instruments

How to classify the financial assets?

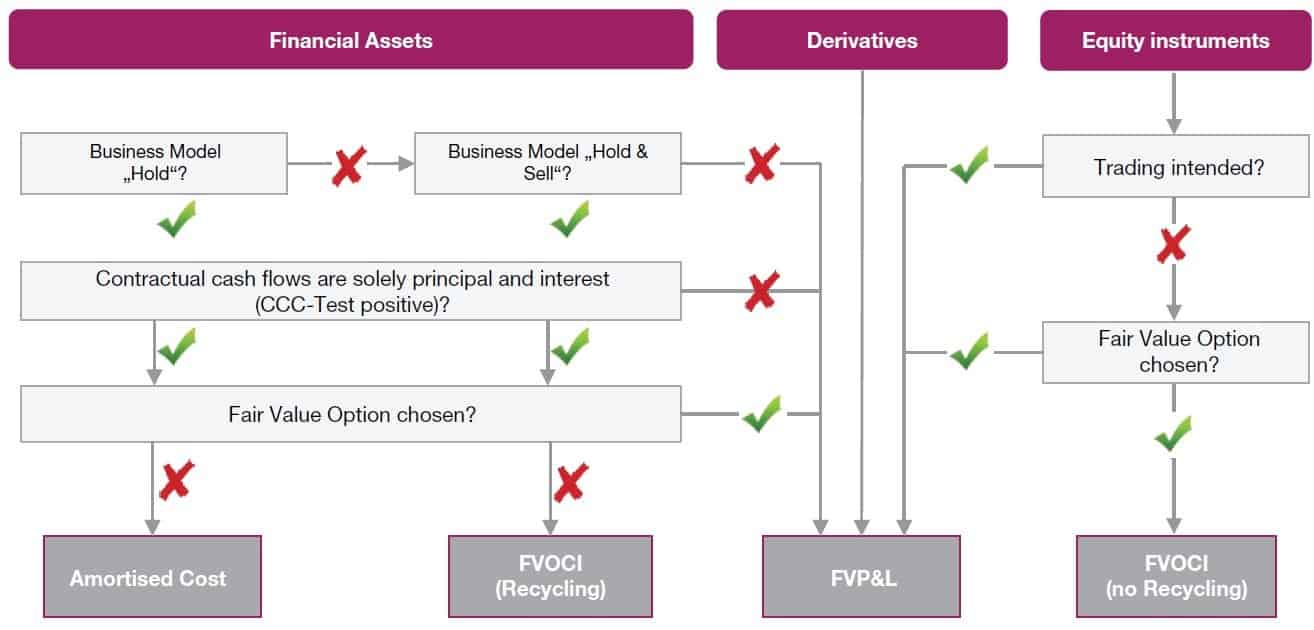

IFRS 9 classifies financial assets based on two characteristics:

-

Business model test

What is the objective of holding financial assets? Collecting the contractual cash flows? Selling? -

Contractual cash flows’ characteristics test

Are the cash flows from the financial assets on the specified dates solely payments of principal and interest on the principal outstanding? Or, is there something else?

Based on these two tests, the financial assets can be classified in the following categories:

Special For You!

Have you already checked out the IFRS Kit ? It’s a full IFRS learning package with more than 40 hours of private video tutorials, more than 140 IFRS case studies solved in Excel, more than 180 pages of handouts and many bonuses included. If you take action today and subscribe to the IFRS Kit, you’ll get it at discount! Click here to check it out!

-

At amortized cost

A financial asset falls into this category if BOTH of the following conditions are met:- Business model test is met, i.e. you hold the financial assets only to collect contractual cash flows (not to sell them), and

- Contractual cash flows’ characteristics test is met, i.e. the cash flows from the asset are only the payments of principal and interest.

Examples: debt securities, receivables, loans.

-

At fair value through other comprehensive income (FVOCI)

Here, there are 2 subcategories:- 2a. If a financial asset meets contractual cash flows characteristics test (i.e. debt assets only) and the business model is to collect contractual cash flows AND SELL financial assets, then such an asset mandatorily falls into this category (unless FVTPL option is chosen; see below)

- 2b. You can voluntarily choose to measure some equity instruments at FVOCI. This is an irrevocable election at initial recognition.

-

At fair value through profit or loss (FVTPL)

All other financial assets fall in this category.

Derivative financial assets are automatically classified at FVTPL.

Moreover, regardless above 2 categories, you may decide to designate the financial asset at fair value through profit or loss at its initial recognition.

The following scheme explains it:

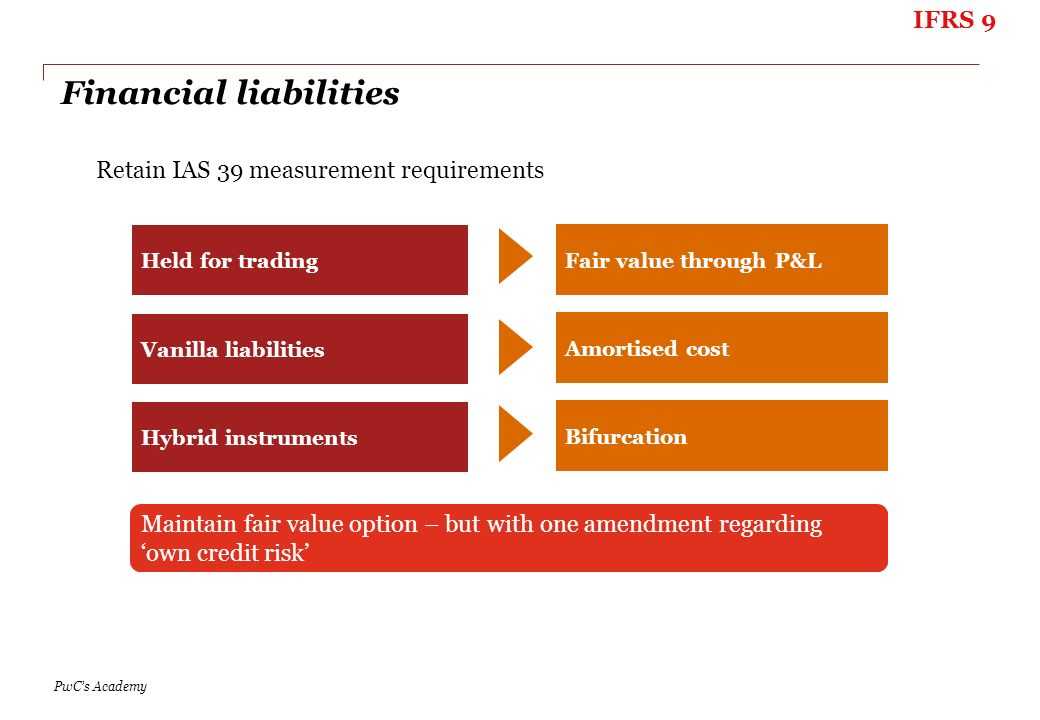

How to classify financial liabilities?

IFRS 9 classifies financial liabilities as follows:

- Financial liabilities at fair value through profit or loss: these financial liabilities are subsequently measured at fair value and here, all derivatives belong.

- Other financial liabilities measured at amortized cost using the effective interest method.

IFRS 9 mentions separately some other types of financial liabilities measured in a different way, such as financial guarantee contracts and commitments to provide a loan at a below market interest rate, but here, we will deal with 2 main categories.

Why IFRS 9?

IFRS 9 establishes principles for the financial reporting of financial assets and financial liabilities.

Please note that:

- IFRS 9 does NOT define financial instruments. You can find the definitions of financial instruments in IAS 32 Financial Instruments: Presentation.

- IFRS 9 does NOT deal with your own (issued) equity instruments like your own shares, issued warrants, written options for equity, etc.

- IFRS 9 DOES deal with the equity instruments of someone else, because they are financial assets from your point of view.

- IFRS 9 does NOT deal with your investments in subsidiaries, associates and joint ventures (look to IFRS 10, IAS 28 and related).

Признание, оценка и учет

Пройдите наш авторский курс по выбору акций на фондовом рынке → обучающий курс

Бесплатный Экспресс-курс «Оценка инвестиционных проектов с нуля в Excel» от Ждановых. Получить доступ

IFRS 9 устанавливает порядок признания, оценки и учета финансовых инструментов. Данным правилам должны придерживаться все международные компании, действующие на территории РФ.

Признание

Признание обязательства либо актива происходит в момент подписания договора, то есть на дату приобретения финансового инструмента, возникновения кредитных обязательств и т.п.

Первичная оценка

Первичная оценка обязательств или активов осуществляется в момент их признания по справедливой стоимости. В зависимости от вида финансового инструмента, затраты, связанные с его приобретением, либо включаются в общую массу, либо исключаются из нее. Траты по обязательствам вычитаются из их стоимости, а затраты по активам, наоборот, приобщаются к объему их денежного выражения.

К расходам, связанным с приобретением финансового инструмента (актива или обязательства), относят следующие затраты:

- Оформление и сопровождение сделки юристами, в том случае, если привлекается сторонняя организация.

- Оплата труда третьих лиц, участвующих в сделке, например торговых агентов или брокеров, в том числе внутренних сотрудников.

- Исполнение налоговых обязательств, связанных с приобретением финансового инструмента.

Существуют затраты, которые запрещено использовать при оценке активов либо обязательств. К таким расходам можно отнести премии, финансирование, хранение инструментов, а также затраты, связанные с содержанием административного комплекса.

Оценка активов и обязательств, принятых по амортизируемой стоимости

Оценка активов, принятых по амортизированной стоимости, производится с учетом их обесценения. Для этого используют следующую формулу:

БСА – ДСФО, где

БСА – балансовая стоимость актива;

ДСФО – дисконтированная цена финансовых оборотов будущих периодов.

Обязательства, классифицируемые при первичной оценке по амортизируемому принципу, отражаются в отчетной документации по амортизируемой стоимости. Динамика их объема регистрируется путем занесения в отчет о прибылях и убытках суммы, определенной по методу эффективной ставки процента.

Оценка активов и обязательств, принятых по справедливой стоимости

Активы, принятые по справедливой стоимости, подлежат переоценке каждый отчетный период до полного прекращения их признания. Операции отражаются в отчете о совокупном доходе.

Однако последующие затраты, связанные с динамикой справедливой стоимости актива, например, переоценка курсовой разницы и обесценивание, прописываются в отчете о прибылях и убытках.

Обязательства, которые первоначально были классифицированы по признаку справедливой стоимости, подлежат оценке с помощью их отражения в прибылях и убытках. Когда прекращается признание финансового инструмента, его стоимость переходит в разряд нераспределенной прибыли.

When to derecognize a financial instrument?

In other words, when to remove a financial instrument from your financial statements?

IFRS 9 treats the derecognition of financial assets differently from the derecognition of financial liabilities, so let’s break it down.

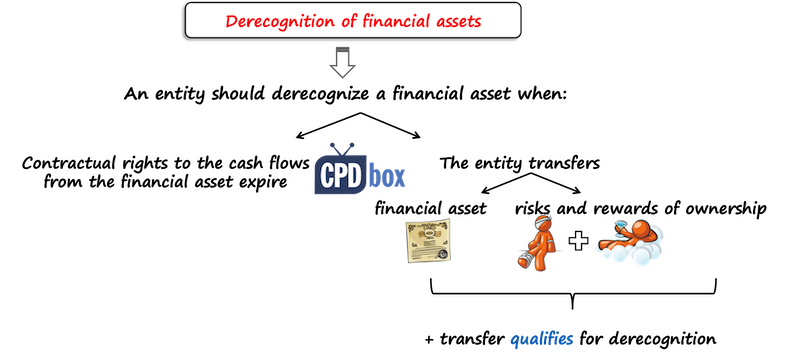

Derecognition of financial assets

While it’s very easy to recognize a financial asset, it’s very difficult and complicated to derecognize it in some cases.

IFRS 9 is very “sticky” and the reason is to prevent companies from hiding toxic assets out of their balance sheets.

Before you decide whether to derecognize or not, you need to determine WHAT you’re dealing with (IFRS 9 par. 3.2.2):

- A financial asset (or a group of similar financial assets) in its entirety, or

- A part of a financial asset (or a part of a group of similar financial assets) meeting specified conditions.

After you determine WHAT you derecognize, then you need derecognize the asset when (IFRS 9 par. 3.2.3):

- The contractual rights to the cash flows from the financial asset expire – that’s an easy and clear option; or

- An entity transfers the financial asset and the transfer qualifies for the derecognition – that’s more complicated.

Transfers of financial assets are discussed in more details and to sum it up, you need to go through the following steps:

- Decide whether the asset (or its part) was transferred or not,

- Determine whether also risks and rewards from the financial asset were transferred.

- If you have neither retained nor transferred substantially all of the risks and rewards of the asset, then you need to assess whether you have retained control of the asset or not.

Transfers of financial assets are then discussed in much greater detail in IFRS 9 and also, application guidance summarizes the derecognition steps in a simple decision tree. You can familiarize yourself with the decision tree in the video below this summary.

Derecognition of a financial liability

An entity shall derecognize a financial liability when it is extinguished.

It happens when the obligation specified in the contract is discharged, cancelled or expires.

Обесценивание

Перед составлением финансовой отчетности стоит подсчитать общий ожидаемый объем кредитных убытков для всех активов, арендной задолженности (дебиторской), обязательств по даче займа и финансовых гарантий.

Существует два метода обесценивания активов и обязательств: общий и упрощенный. Первый прием заключается в признании убытков в соответствии с этапом, на котором в момент обесценения находится финансовый инструмент. Различают 3 стадии:

- Резерв под убытки признается равным одному году. В таком случае активы называют надежными.

- Резерв создается на весь срок действия актива. В таком случае инструмент называют предметом повышенного риска.

- Для полностью обесценившихся активов необходимо признать убыточный резерв в полном объеме, а доход или затраты отразить по принципу амортизируемой стоимости.

Второй прием более простой. Упрощенная модель не подразумевает определения этапа финансового инструмента. Резерв всегда принимается в полном объеме.