Presentation in financial statements

IAS 21 does not specify in which part of the income statement foreign exchange differences should be presented. Therefore, entities must develop an accounting policy. The most common approach is to report exchange differences in the same section of the income statement where the original income or expense was (or will be) recognised for the item that subsequently led to exchange differences. For example, exchange differences on trade receivables are presented within operating profit, while exchange differences on debt are presented within finance costs. This method aligns with the one proposed by the IASB in their primary financial statements project.

Translating a foreign operation

When an entity within a group uses a different presentation currency from that of the consolidated financial statements, translations are performed using the following procedures as per IAS 21.39:

- Assets, including goodwill and fair value adjustments (IAS 21.47), and liabilities, are translated at the closing rate at the reporting date. This includes comparatives translated using historical rates.

- Income and expenses are translated at exchange rates applicable at the transaction dates. This also includes comparatives translated using historical rates.

- All resulting exchange differences are recognised in other comprehensive income (OCI).

IAS 21.40 allows for simplifications in determining the foreign exchange rate, for example, using an average rate, assuming exchange rates do not significantly fluctuate. In practice, an average rate for each month is most commonly used.

Cumulative translation adjustment (CTA)

Exchange differences referred to in IAS 21.39(c) are commonly identified as either ‘Cumulative Translation Adjustment’ (CTA) or ‘Foreign Currency Translation Reserve’ (FCTR). The two primary sources for CTA, as per IAS 21.41, include:

- Translating income and expenses at the transaction date exchange rates, while assets and liabilities are translated at the closing rate.

- Translating opening assets and liabilities at a closing rate that differs from the opening rate.

CTA is recognised in OCI, presented as a distinct item within equity, and not recycled to P/L until the foreign operation is disposed of. CTA is further divided between controlling and non-controlling interests (IAS 21.41). It is also recognised in OCI for investments accounted for using the equity method (IAS 21.44).

Consider Group A with the Euro as its presentation currency. Entity X, one of Group A’s subsidiaries, uses the US Dollar as its presentation currency. The following EUR/USD exchange rates apply:

- Opening rate at 1 January 20X1: 1.1

- Average rate in 20X1: 1.2

- Closing rate at 31 December 20X1: 1.3

All calculations and tables presented in this example can be downloaded in an Excel file.

Entity X is consolidated to Group A consolidated financial statements as follows:

Entity X stand-alone data

Statement of financial position in USD:

P/L in USD:

Consolidation of Group A

Consolidated statement of financial position in EUR at 1 January 20X1:

Consolidated statement of financial position in EUR at 31 December 20X1:

Consolidated P/L for 20X1 in EUR:

Intragroup balances

Exchange differences on intragroup balances

Although intragroup balances are eliminated during consolidation, any exchange differences arising from those balances are not. This is because the group is effectively exposed to foreign exchange gains and losses, even on intragroup transactions, including dividend receivables and payables (IAS 21.45).

Goodwill considerations

Goodwill, as previously stated, is considered an asset of a foreign operation and is retranslated at each reporting date. For multinational group acquisitions, goodwill should be allocated to each functional currency level of the acquired foreign operation (IAS 21.BC32).

Net investment in a foreign operation

A net investment in a foreign operation represents the reporting entity’s interest in the net assets of that operation (IAS 21.8). Monetary items receivable from, or payable to, a foreign operation, where settlement is neither planned nor likely to occur in the foreseeable future, are treated as part of the entity’s net investment in that operation (IAS 21.15-15A). Exchange differences arising from such monetary items are recognised in P/L in separate financial statements, but in OCI (as part of CTA) in consolidated financial statements (IAS 21.32-33).

Disposal or partial disposal of a foreign operation

Upon disposing of a foreign operation, the cumulative amount of exchange differences relating to that operation, recognised in OCI and accumulated in the separate component of equity (i.e. CTA), is reclassified from equity to P/L (as a ) when the gain or loss on disposal is recognised (IAS 21.48). Furthermore, paragraph IAS 21.48A outlines accounting procedures for partial disposals.

IAS 21.42-43 provides specific provisions for translating from the currency of a hyperinflationary economy.

Проблемы перехода на МСФО

How to translate financial statements into a Presentation Currency

When an entity presents its financial in the presentation currency different from its functional currency, then the rules depend on whether the entity operates in a non-hyperinflationary economy or not.

Non-hyperinflationary economy

When an entity’s functional currency is NOT the currency of a hyperinflationary economy, then an entity should translate:

- All assets and liabilities for each statement of financial position presented (including comparatives) using the closing rate at the date of that statement of financial position.

Here, this rule applies for goodwill and fair value adjustments, too. - All income and expenses and other comprehensive income items (including comparatives) using the exchange rates at the date of transactions.

Standard IAS 21 permits using some period average rates for the practical reasons, but if the exchange rates fluctuate a lot during the reporting period, then the use of averages is not appropriate.

All resulting exchange differences shall be recognized in other comprehensive income as a separate component of equity.

However, when an entity disposes the foreign operation, then the cumulative amount of exchange differences relating to that foreign operation shall be reclassified from equity to profit or loss when the gain or loss on disposal is recognized.

Hyperinflationary economy

When an entity’s functional currency IS the currency of a hyperinflationary economy, then the approach slightly changes:

- The entity’s current year’s financial statements are restated first, as required by IAS 29 Financial Reporting in Hyperinflationary Economies. Comparative figures are used the same as current year’s figures in the financial statements from previous reporting period.

- Only then, the same procedures as described above are applied.

IAS 21 prescribes the number of disclosures, too. Please watch the following video with the summary of IAS 21 here:

Have you ever been unsure what foreign exchange rate to use? Please comment below this video and don’t forget to share it with your friends by clicking HERE. Thank you!

Отражение в функциональной валюте

Когда заключается сделка в валюте, отличной от её функциональной валюты, производится пересчет статей в иностранной валюте в свою функциональную валюту и отражается последствия такого пересчета в финансовой отчетности.

При первоначальном признании в функциональной валюте операции в иностранной валюте учитываются путем применения к сумме в иностранной валюте текущего валютного курса между функциональной валютой и иностранной валютой на дату совершения операции.

На каждые последующие отчетные даты пересчитываются:

- монетарные статьи с учетом курса закрытия

- немонетарные статьи в иностранной валюте, учтенные по исторической стоимости, пересчитываются по обменному курсу на дату осуществления операции

- немонетарные статьи в иностранной валюте, оцененные по справедливой стоимости, пересчитываются по обменным курсам, действовавшим на дату определения справедливой стоимости.

Курсовые разницы подлежат признанию в прибыли или убытке в том периоде, в котором они возникают.

Результаты и финансовые показатели компании, чья функциональная валюта не является валютой гиперинфляционной экономики, подлежат пересчету в другую валюту представления с использованием следующих процедур:

- активы и обязательства пересчитываются по курсу закрытия на конец периода

- доходы и расходы пересчитываются по курсам на даты осуществления операций

- все возникшие курсовые разницы признаются в качестве отдельного компонента капитала.

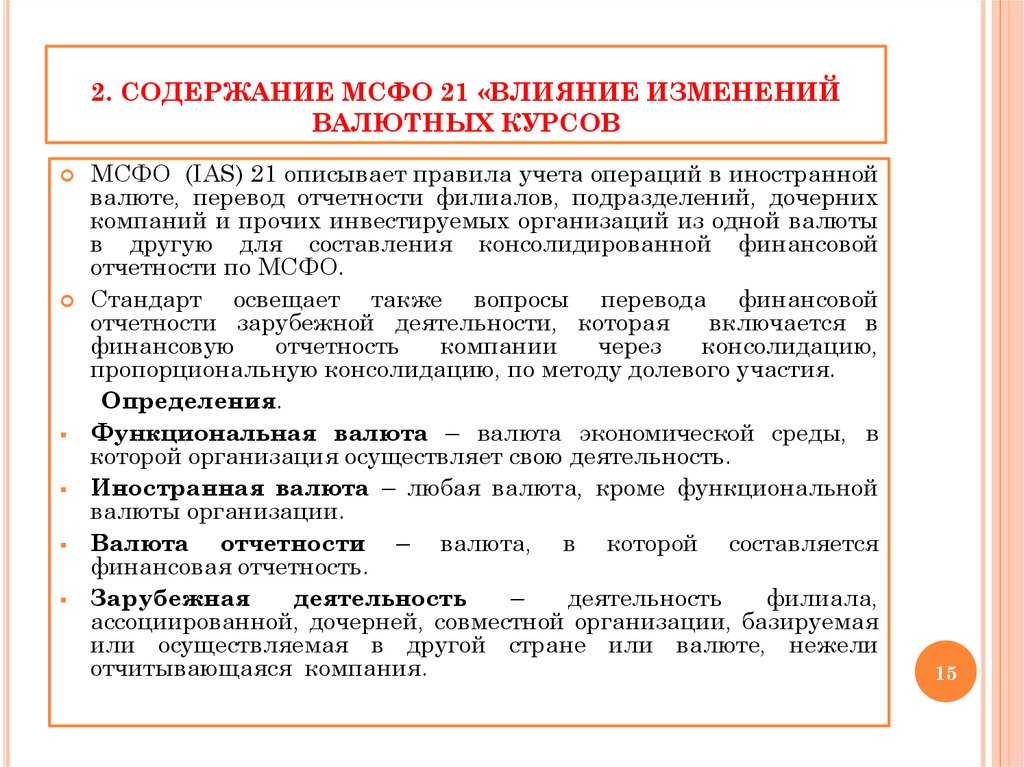

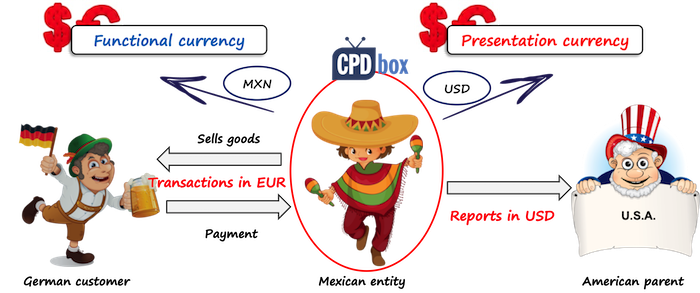

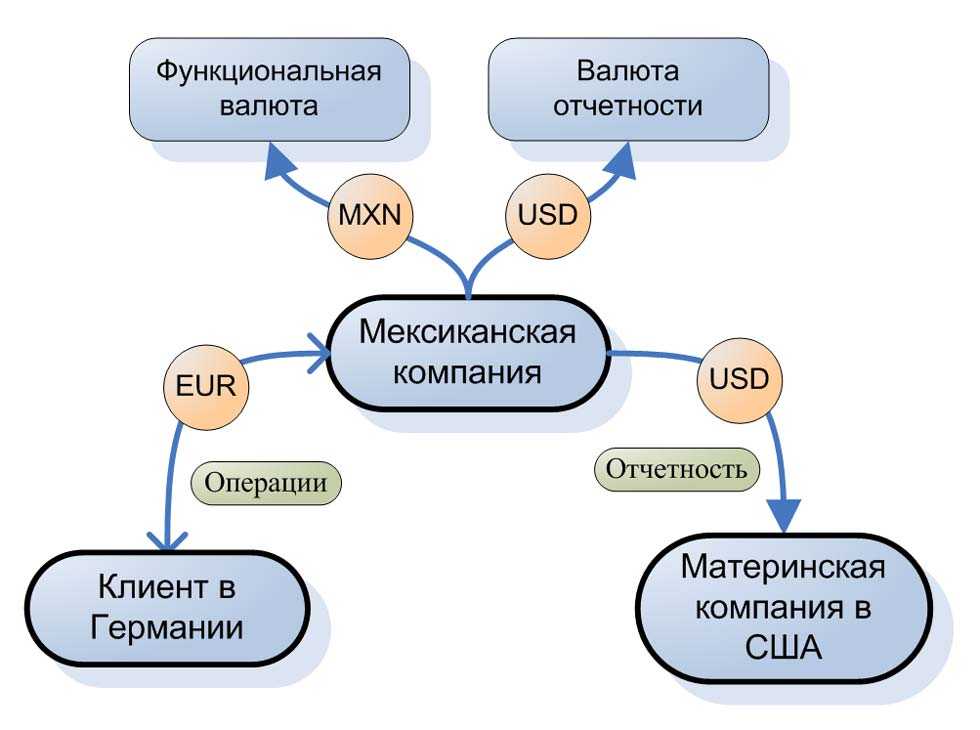

Functional vs. Presentation Currency

IAS 21 defines both functional and presentation currency and it’s crucial to understand the difference:

Functional currency is the currency of the primary economic environment in which the entity operates. It is the own entity’s currency and all other currencies are “foreign currencies”.

Presentation currency is the currency in which the financial statements are presented.

In most cases, functional and presentation currencies are the same.

Special For You!

Have you already checked out the IFRS Kit ? It’s a full IFRS learning package with more than 40 hours of private video tutorials, more than 140 IFRS case studies solved in Excel, more than 180 pages of handouts and many bonuses included. If you take action today and subscribe to the IFRS Kit, you’ll get it at discount! Click here to check it out!

Also, while an entity has only 1 functional currency, it can have 1 or more presentation currencies, if an entity decides to present its financial statements in more currencies.

You also need to realize that an entity can actually choose its presentation currency, but it CANNOT choose its functional currency. The functional currency needs to be determined by assessing several factors.

How to determine functional currency

The most important factor in determining the functional currency is the entity’s primary economic environment in which it operates. In most cases, it will be the country where an entity operates, but this is not necessarily true.

The primary economic environment is normally the one in which the entity primarily generates and expends the cash. The following factors can be considered:

- What currency does mainly influence sales prices for goods and services?

- In what currency are the labor, material and other costs denominated and settled?

- In what currency are funds from financing activities generated (loans, issued equity instruments)?

- And other factors, too.

Sometimes, sales prices, labor and material costs and other items might be denominated in various currencies and therefore, the functional currency is not obvious.

In this case, management must use its judgment to determine the functional currency that most faithfully represents the economic effects of the underlying transactions, events and conditions.

How to report transactions in Functional Currency

Initial recognition

Initially, all foreign currency transactions shall be translated to functional currency by applying the spot exchange rate between the functional currency and the foreign currency at the date of the transaction.

The date of transaction is the date when the conditions for the initial recognition of an asset or liability are met in line with IFRS.

Subsequent reporting

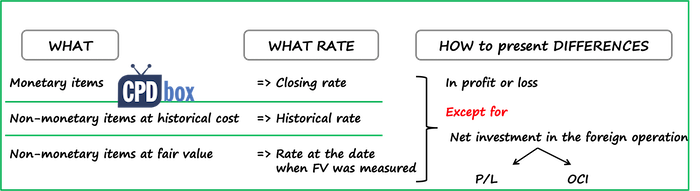

Subsequently, at the end of each reporting period, you should translate:

- All monetary items in foreign currency using the closing rate;

- All non-monetary items measured in terms of historical cost using the exchange rate at the date of transaction (historical rate);

- All non-monetary items measured at fair value using the exchange rate at the date when the fair value was measured.

How to report foreign exchange differences

All exchange rate differences shall be recognized in profit or loss, with the following exceptions:

- Exchange rate gains or losses on non-monetary items are recognized consistently with the recognition of gains or losses on an item itself.For example, when an item is revalued with the changes recognized in other comprehensive income, then also exchange rate component of that gain or loss is recognized in OCI, too.

- Exchange rate gain or loss on a monetary item that forms a part of a reporting entity’s net investment in a foreign operation shall be recognized:

- In the separate entity’s or foreign operation’s financial statements: in profit or loss;

- In the consolidated financial statements: initially in other comprehensive income and subsequently, on disposal of net investment in the foreign operation, they shall be reclassified to profit or loss.

Change in functional currency

When there is a change in a functional currency, then the entity applies the translation procedures related to the new functional currency prospectively from the date of the change.

Слайд 10МСФО (IAS) 21. Влияние изменений валютных курсов.ВЛИЯНИЕ ГИПЕРИНФЛЯЦИИК финансовой отчетности

зарубежной компании, отчитывающейся в валюте страны, с гиперинфляционной экономикой до

перевода в валюту отчетности в обязательном порядке применяются положения МСФО 29 («Финансовая отчетность в условиях гиперинфляции»).Далее (после корректировки на гиперинфляции согласно положениям МСФО 29) активы и обязательства каждого представляемого бухгалтерского баланса и статьи отчета о прибыли и убытках (включая сравнительные данные) пересчитываются по курсу, действующему на дату составления отчетности.При наступлении условий прекращения применения положения МСФО 29 в качестве первоначальной стоимости для последующего пересчета в валюту отчетности принимаются остатки на дату последней отчетности (когда последний раз применялись положения МСФО 29).

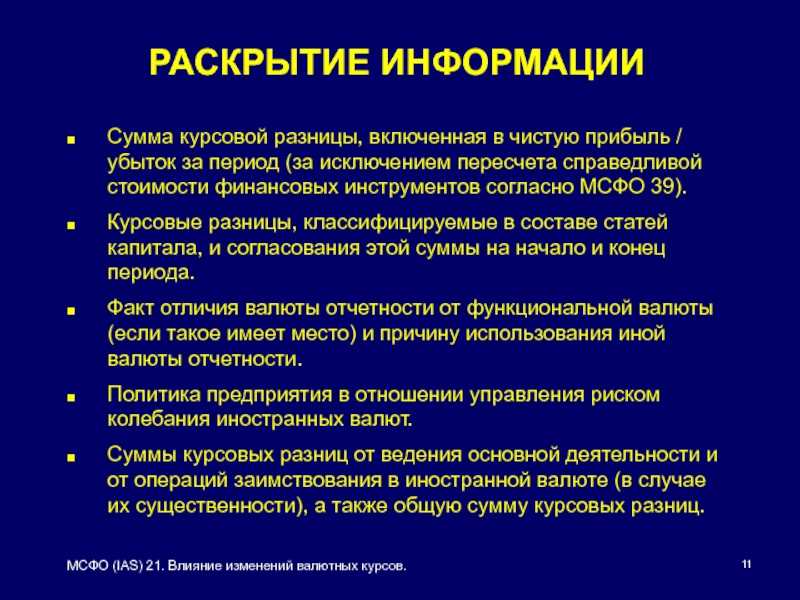

Слайд 11МСФО (IAS) 21. Влияние изменений валютных курсов.РАСКРЫТИЕ ИНФОРМАЦИИСумма курсовой разницы,

включенная в чистую прибыль / убыток за период (за исключением

пересчета справедливой стоимости финансовых инструментов согласно МСФО 39).Курсовые разницы, классифицируемые в составе статей капитала, и согласования этой суммы на начало и конец периода.Факт отличия валюты отчетности от функциональной валюты (если такое имеет место) и причину использования иной валюты отчетности.Политика предприятия в отношении управления риском колебания иностранных валют.Суммы курсовых разниц от ведения основной деятельности и от операций заимствования в иностранной валюте (в случае их существенности), а также общую сумму курсовых разниц.

МСФО, Дипифр

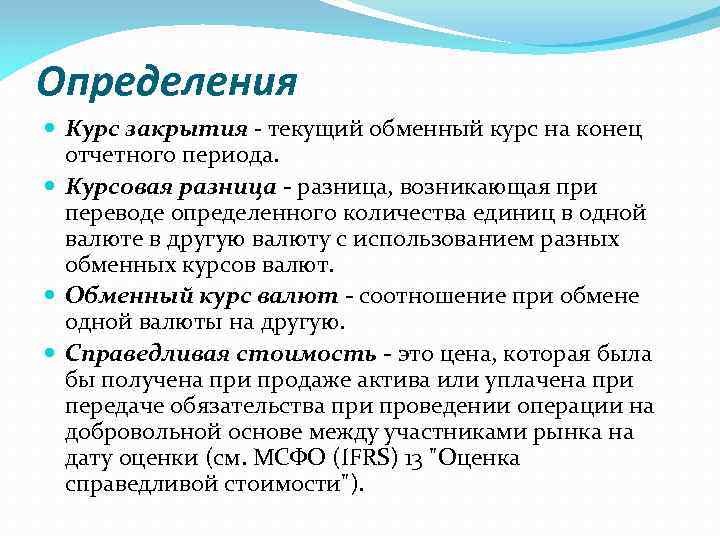

Курсовые разницы — это разницы, возникающие при пересчете стоимости активов/обязательств из одной валюты в другую. Они неизбежно возникают, так как обменные курсы валют постоянно меняются.

Бухгалтерский учет операций в иностранной валюте регулируется международным стандартом МСФО (IAS) 21 «Влияние изменений валютных курсов». В российском учете эти операции регламентируются в ПБУ 3/2006.

МСФО 21 вводит понятия монетарных и немонетарных статей баланса, функциональной валюты и валюты представления, которые отсутствуют в ПБУ 3/2006 в силу более узкой сферы применения, а также отличающихся учетных правил.

Читайте ниже в данной статье:

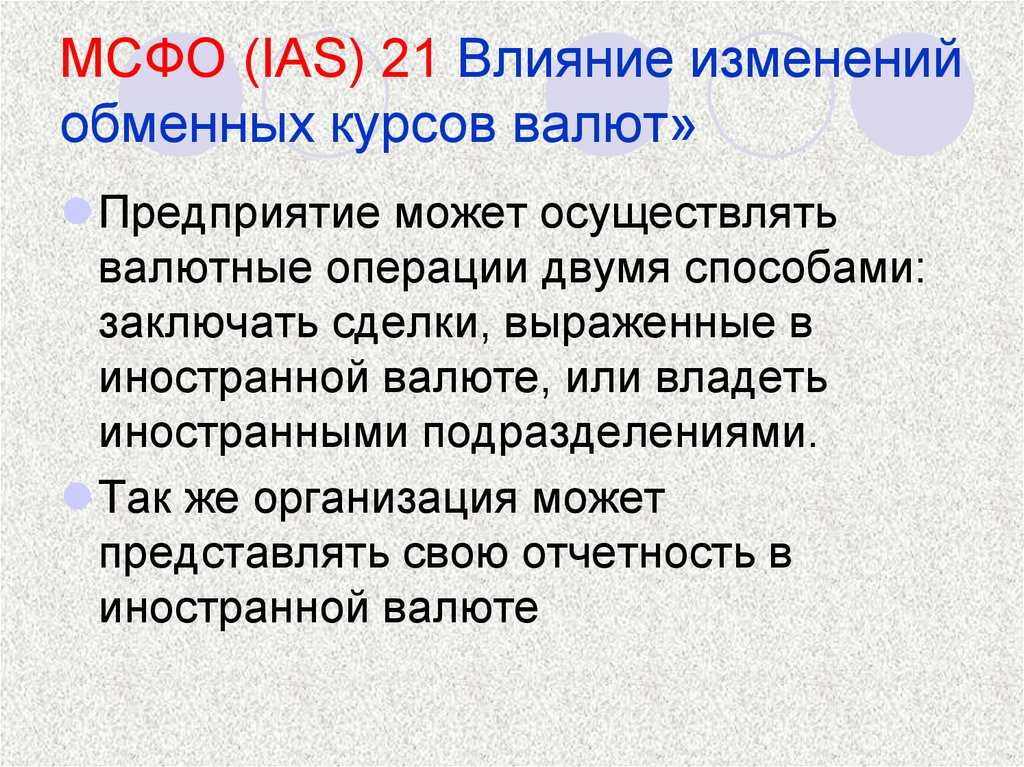

МСФО (IAS) 21 применяется для бухгалтерского учета валютных операций в следующих случаях:

- если компания совершает сделки в иностранной валюте (и имеет активы и обязательства, деноминированные в валюте) (примеры)

- если компания приняла решение о подготовке консолидированной отчетности в иностранной валюте (для России это может быть отчетность по МСФО в долларах или евро) (пример)

- если компания имеет зарубежное подразделение и необходимо предоставлять результаты деятельности этого подразделения в национальной валюте

Сфера применения российского ПБУ 3/2006 распространяется только на индивидуальную отчетность организации при пересчете операций в российские рубли, т.е. не включает пункты 2 и 3 из вышеприведенного списка.

В МСФО курсовые разницы могут относиться как на прибыли и убытки, так и на прочий совокупный доход.

В РСБУ курсовые разницы отражаются проводками в корреспонденции с 91 счетом:

- Дт 50, 52, 55, 57, 60, 62, 66, 67, 76 Кт 91-1 — положительная курсовая разница

- Дт 91-2 Кт 50, 52, 55, 57, 60, 62, 66, 67, 76 — отрицательная курсовая разница

Функциональная валюта и валюта представления

Функциональная валюта — это валюта, используемая в основной экономической среде, в которой компания осуществляет свою деятельность. Для российских компаний, которые совершают продажи и покупки в рублях, выплачивают зарплату и берут кредиты в рублях функциональной валютой является рубль.

Иностранная валюта— любая валюта, отличная от функциональной валюты предприятия.

Валюта представления отчетности — это валюта, в которой представляется финансовая отчетность.

Если российская компания готовит консолидированную финансовую отчетность по МСФО в долларах, то доллар является валютой представления отчетности.

В этом случае необходимо сделать пересчет всех статей баланса и отчета о прибылях и убытках из рублей (функциональная валюта) в доллары (валюта представления). Как это сделать, прописано в МСФО 21.

Два основных вопроса, которые возникают в связи с учетом валютных операций:

- 1) какой обменный курс применять при пересчете валют

- 2) где отразить курсовые разницы в отчетности.

Для ответа эти вопросы МСФО 21 разделяет статьи баланса на монетарные и немонетарные.

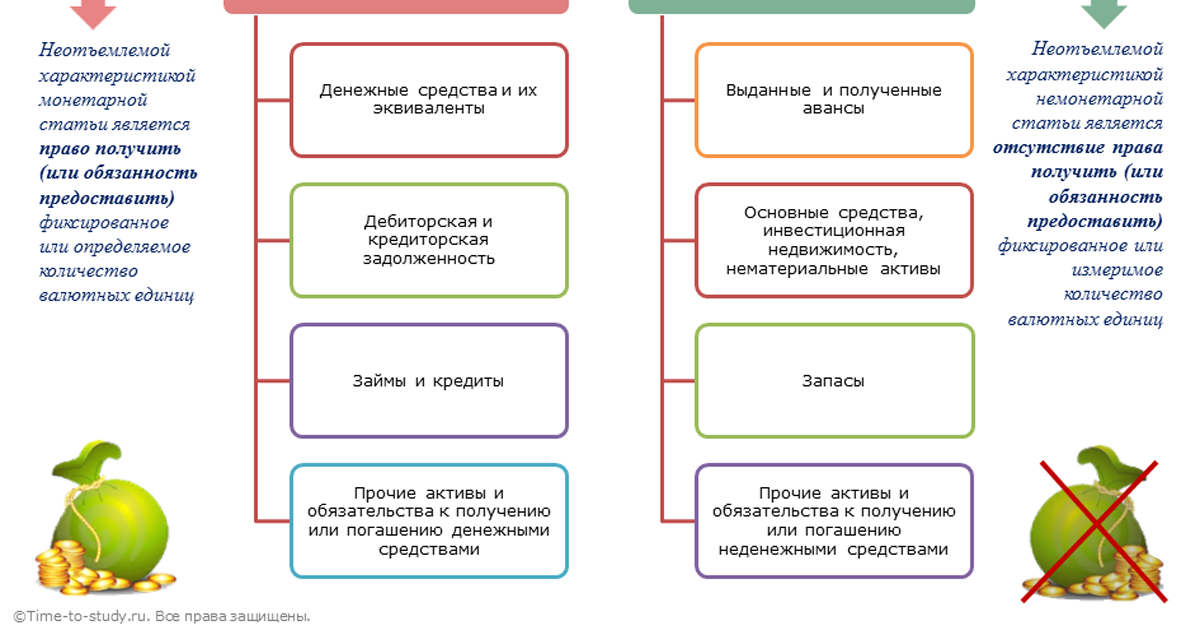

Монетарные и немонетарные статьи

Монетарные статьи – это а) денежные средства в валюте или б) активы и обязательства, которые подлежат получению или выплате денежными средствами. Монетарными статьями являются дебиторская и кредиторская задолженности, финансовые инструменты, выраженные в иностранной валюте.

К немонетарным статьям относятся, основные средства, нематериальные активы, запасы, гудвил, авансы выданные и авансы полученные и расчетные обязательства, расчет по которым должен быть произведен путем предоставления немонетарного актива. Авансы выданные/полученные (например, предоплата за аренду) согласно МСФО 21 относятся к немонетарным активам, поскольку погашаются не денежными средствами, а услугами или товарами.

Примеры расчета курсовой разницы — из иностранной валюты в функциональную

Обменный курс рубля к доллару ЦБ РФ:

- 15 декабря 2014 — 58,3461

- 31 января 2015 — 68,9291

Пример 1. Монетарный актив

Допустим, вы купили 1,000 долларов 15 декабря 2014 года по курсу 58,3461 за сумму 58,346.1 рублей. Через 1,5 месяца 31 января 2015 года обменный курс рубля к доллару существенно вырос, и $1,000 теперь стоят 68,929.1 рублей. Разница между стоимостью покупки и суммой оценки на 31 января составляет 10,583 рубля.

Это и есть курсовая разница по операции покупки валюты. В данном случае это курсовая прибыль (положительная курсовая разница), так как стоимость нашего актива (денежные средства) выросла из-за роста курса доллар.

Если бы мы продали $1,000 31 января 2015, то эта прибыль бы реализовалась: мы бы получили на 10,583 рубля больше, чем заплатили за доллары в середине декабря 2014.

15.12.14 Дт Денежные средства (валюта) Кт Денежные средства (рубли) — 58,346.1

Functional and foreign currencies

Defining functional and foreign currencies

The functional currency is defined as the currency of the primary economic environment in which an entity operates, i.e. primarily generates and spends cash. IAS 21.9-10 details the factors that should be considered in determining an entity’s functional currency.

The foreign currency, as defined by IAS 21.8, is any currency that is different from the entity’s functional currency.

Functional currency of a foreign operation

Identifying the functional currency can be particularly complex when a reporting entity is a foreign operation of another entity and fundamentally an extension of its operations. For instance, a ‘financial’ subsidiary (i.e., a subsidiary primarily holding financial assets or issuing debt) whose core financial assets and liabilities are denominated in the parent’s functional currency may have the same functional currency as the parent, regardless of its operational country. IAS 21.11 outlines additional factors to be considered when determining the functional currency of a foreign operation. If these indicators are mixed, priority is given to the primary indicators described in IAS 21.9.

Выводы и заключение

Стандарт «IAS 21 Влияние изменений курсов валют» – прикладной инструмент финансовых менеджеров организаций, который помогает компаниям формировать качественную финансовую отчетность вне зависимости от операционных различий финансовых расчетов группы компаний на разных рынках

Для внешних пользователей применение положений стандарта особенно важно, поскольку позволяет сформировать пакет отчетности по компании, максимально корректно отражающий финансовое состояние с учетом влияния валютных факторов. Сегодня валютный фактор признается по всему миру как один из самых главных для коммерческих компаний ввиду широкого диапазона волотильности валютных пар и большой зависимости курсовых значений от внешних макроэкономических и политических данных

Такой инструмент, как стандарт МСФО 21, позволяет максимально стандартизировать валютные сведения в целом по компании и представить пользователям корректные обобщенные данные для дальнейшей управленческой и аналитической работы.